Ever found yourself paying a friend back for coffee with a tap on your phone, investing your spare change from a grocery run, or getting a loan approved in minutes without ever talking to a banker? If you’ve done any of these things, congratulations—you’re already an active citizen in the new digital financial world. You’re living in the FintechZoom.com Economy.

It’s a term you might have seen floating around, but what does it actually mean for you and your finances? It’s more than just a buzzword; it’s a fundamental shift in how we think about, move, and grow our money. Let’s break it down together, in plain English.

What Exactly is the FintechZoom.com Economy?

Think of the traditional economy like a grand, old-fashioned library. It’s full of valuable information (money), but you have to go through specific channels (bank tellers, brokers), follow strict hours, and navigate a lot of red tape to get what you need.

Now, imagine that library got a revolutionary upgrade. Every book is now digitally available on your personal device, you can get personalized reading recommendations instantly, and you can share resources with anyone in the world seamlessly. That’s the FintechZoom Economy.

In simple terms, the FintechZoom Economy is the ecosystem of financial activities—saving, investing, borrowing, and spending—that is powered by digital technology, innovative software, and a user-first approach. It’s not about building more brick-and-mortar banks; it’s about building smarter, faster, and more accessible financial tools in the palm of your hand.

How the FintechZoom.com Economy Actually Works: A Peek Under the Hood

This new economy doesn’t run on magic. It’s built on a few key technological pillars that work together to create a smooth experience:

- Digital Banking and Payments: This is the most visible part. Apps from digital-only banks and mobile payment services have cut the cord from traditional banks. They allow for instant transactions, lower fees, and budgeting tools that update in real-time.

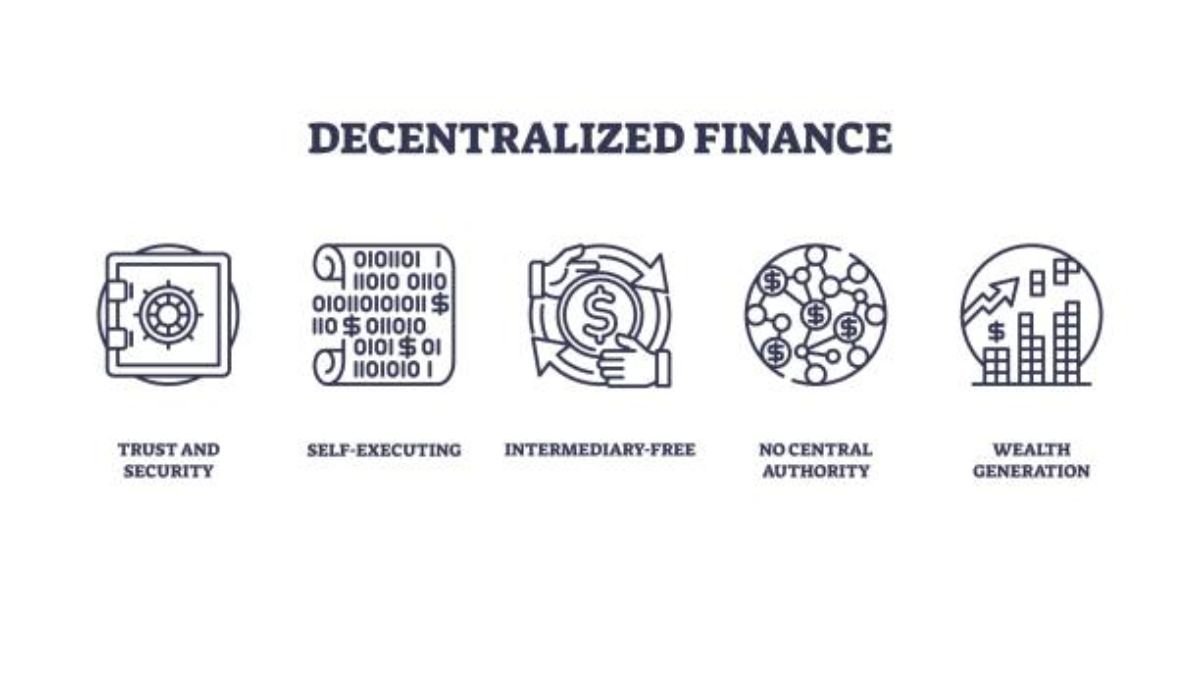

- Blockchain and Cryptocurrency: This is the backbone for trust and transparency. Imagine a public, unchangeable ledger that records every transaction. That’s blockchain. It allows for digital currencies to exist and enables things like “smart contracts” that execute automatically, removing the need for a middleman.

- Artificial Intelligence (AI) and Machine Learning: This is the brain. AI algorithms analyze your spending habits to detect fraud, offer personalized financial advice through automated services, and assess credit risk more accurately than old-fashioned metrics ever could.

- Big Data: This is the fuel. By safely and securely analyzing vast amounts of data, fintech companies can understand economic trends, personalize user experiences, and create products that people actually need.

Real-Life Impact: How This Digital Economy Touches Your Wallet

Okay, so the tech is cool, but how does it help you? Let’s look at a direct comparison.

| Scenario | Traditional Economy Experience | FintechZoom Economy Experience |

| Sending Money Internationally | Go to a bank branch, fill out forms, pay high fees, and wait 3-5 business days. | Use a money transfer app, get the real exchange rate, pay a low, transparent fee, and see the money arrive in hours. |

| Investing $100 | Call a broker, pay a hefty commission, and be limited to whole shares of expensive stocks. | Use a micro-investing app, buy fractional shares with zero commission, and start building a diversified portfolio instantly. |

| Getting a Loan | Schedule meetings, provide stacks of paperwork, and wait weeks for a credit decision. | Apply online through a digital lending platform, get a decision based on more than just your credit score, and receive funds in a day or two. |

It’s all about convenience, lower costs, and empowerment. For example, Sarah, a freelance graphic designer, uses a digital-only bank to separate her business and personal finances automatically. John, a recent college grad, uses a micro-investing app to slowly build a nest egg without feeling the pinch.

Q: Is my money safe in this new economy?

A: This is a great and important question. Reputable fintech companies are typically insured for banking products or investing products, just like traditional institutions. The key is to do your research and use established, regulated platforms.

Read also: Fintech Zoom Overview: Your Gateway to Finance Insights

Navigating the Future: What’s Next for the FintechZoom Economy?

The train has left the station, and it’s only picking up speed. Here’s what we can expect next:

- Embedded Finance: You won’t even need a separate banking app. Financial services will be woven into the apps you already use. Think buying a coffee through a retailer’s app and getting a micro-loan to pay for it, all at once.

- Central Bank Digital Currencies (CBDCs): Governments are exploring their own digital currencies, which could make everything from paying taxes to receiving benefits faster and more efficient.

- Hyper-Personalization: Your financial app will act more like a personal CFO, predicting cash flow issues before they happen and suggesting optimizations tailored specifically to your life goals.

The FintechZoom Economy is making finance more democratic, putting powerful tools that were once reserved for the wealthy into everyone’s hands.

Conclusion

The FintechZoom Economy isn’t a distant future concept; it’s here, and it’s reshaping our financial lives for the better by prioritizing speed, accessibility, and user control.

Feeling ready to dive in? Here are 3 actionable steps you can take today:

- Audit One Financial Habit: Look at one recurring payment—like your monthly phone bill. See if a fintech app like a digital bank can offer you cashback or a better way to manage it.

- Try One Micro-Investment: Download a reputable investing app and explore its “fractional share” feature. Invest just $5 in a company you believe in to get a feel for the process.

- Educate Yourself: Follow financial news on platforms that cover this shift to stay informed about new tools and trends.

What’s your experience been like so far? Are you fully on board with digital banking, or are you cautiously dipping a toe in? I’d love to hear your thoughts and questions below!

FAQs

Q: Is the FintechZoom Economy just about cryptocurrency?

A: No, not at all. Cryptocurrency is one component. The economy encompasses all digital financial technologies, including digital banking, online investing, peer-to-peer payments, and insurtech.

Q: Do I have to be tech-savvy to participate?

A: Absolutely not. A core goal of fintech is to simplify finance. Most apps are designed with a clean, intuitive user interface that makes them as easy to use as any social media app.

Q: Are fintech services more expensive than traditional banks?

A: Often, they are significantly less expensive. They have lower overhead costs (no physical branches) and often pass those savings to users through zero fees, lower loan rates, and better exchange rates.

Q: What are the risks?

A: The primary risks are related to cybersecurity and the potential for less regulatory clarity in emerging areas like crypto. Always use strong passwords, enable two-factor authentication, and only use regulated, well-known platforms.

Q: How does this concept help me understand this economy?

A: This concept provides a framework for understanding the news, analysis, and reviews on the latest companies, technologies, and trends, helping you make informed decisions in this rapidly evolving space.

You may also like: Stay Ahead of the Curve: Why FintechZoom.com Crypto News is Your Essential Market Compass